BHP Group (BHP)·H1 2026 Earnings Summary

BHP Delivers Record Copper Half as Earnings Surge 25%, Dividend Jumps 46%

February 16, 2026 · by Fintool AI Agent

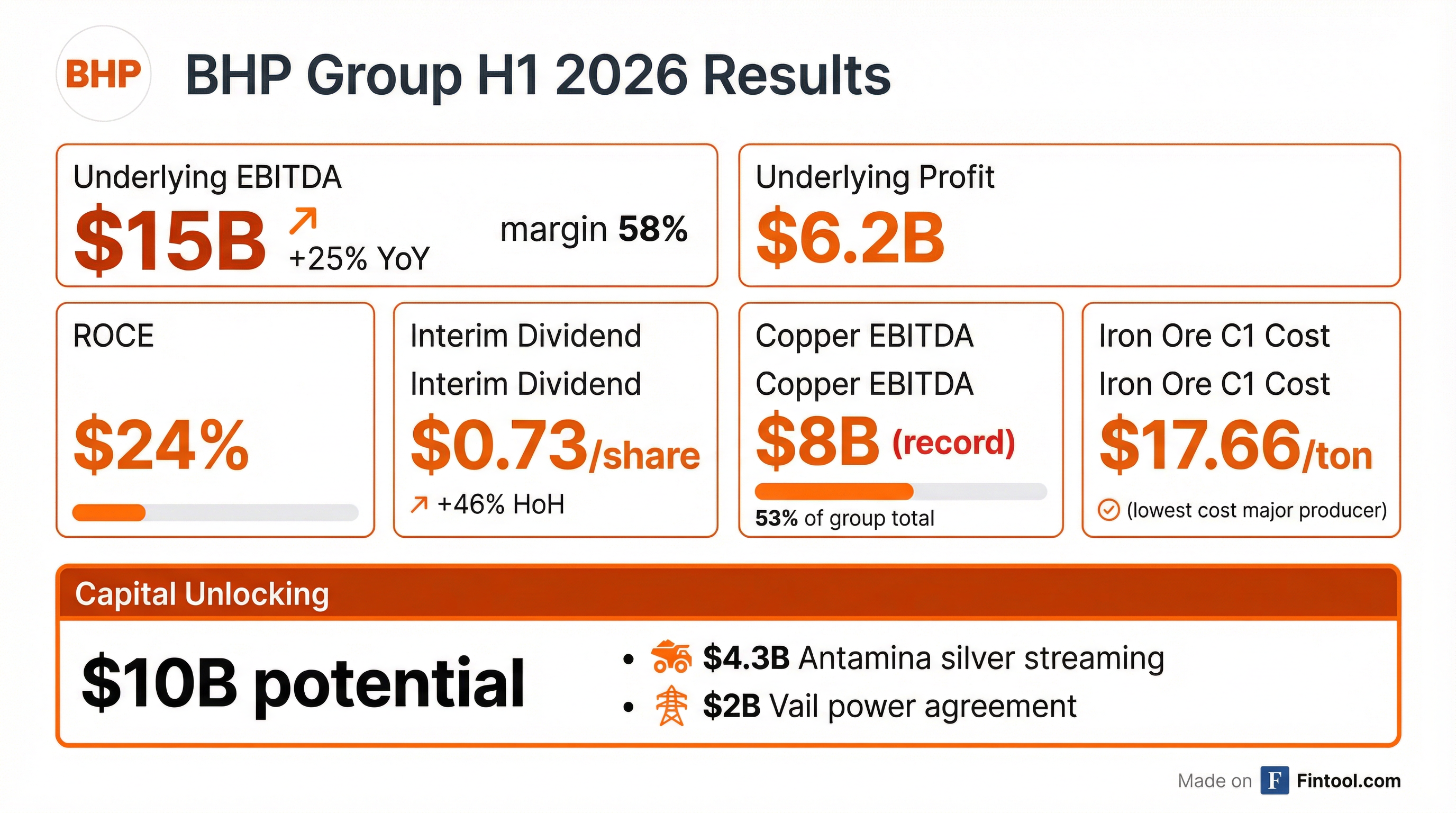

BHP Group delivered a strong first half of fiscal 2026, with underlying EBITDA surging 25% year-over-year to a 58% margin as record copper and iron ore production coincided with elevated commodity prices. The world's largest diversified miner declared an interim dividend of $0.73 per share—up 46% from the prior half—and announced plans to unlock up to $10 billion in capital for reinvestment or shareholder returns.

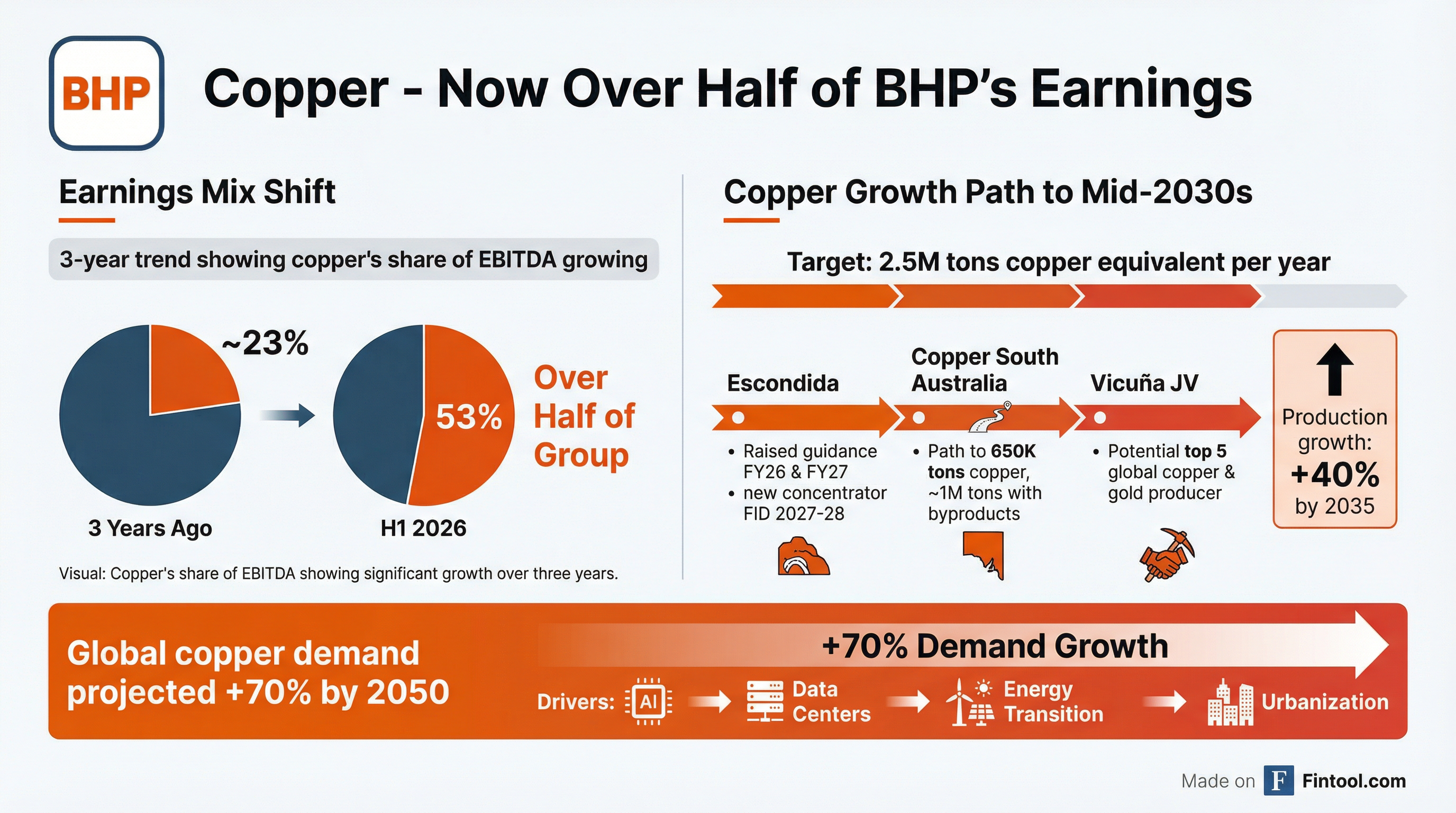

The headline story: copper now generates more than half of BHP's earnings, a strategic milestone that positions the company for the multi-decade growth in copper demand driven by AI, data centers, and the energy transition.

Did BHP Beat Expectations?

BHP reports on a half-yearly basis and doesn't provide formal quarterly guidance, making direct beat/miss analysis less straightforward than U.S. equities. However, the key financial metrics showed significant improvement versus both prior periods:

CEO Mike Henry emphasized the "strong performance on production delivery and cost control, coupled with a strong commodity price environment" as the key drivers.

What Changed From Last Half?

Copper's Dominance Accelerates

The most significant shift: copper now accounts for 53% of BHP's group EBITDA, up 30 percentage points over the past three years. This reflects deliberate portfolio reshaping through:

- More reliable operations at Olympic Dam

- Grade and sequencing optimization at Escondida

- The OZ Minerals acquisition integration

Copper generated a record $8 billion in EBITDA in the half at a 66% margin—the highest in the group's commodity portfolio.

$10 Billion Capital Unlocking Initiative

Management announced a significant capital reallocation strategy, identifying up to $10 billion that could be unlocked from existing assets and reinvested or returned to shareholders:

CFO Vandita Pant described the Antamina deal as "the most valuable ever silver streaming agreement," generating nearly the full value of BHP's share of Antamina while retaining full copper exposure.

Escondida Guidance Raised Again

BHP raised production guidance at Escondida for both FY26 and FY27, now targeting 1.0-1.1 million tons for FY27—a cumulative 150,000 ton increase over the next two years.

The company now expects to deliver over 500,000 more tons over the next five years compared to projections from the 2024 Chile site visit. At current prices and margins, this represents an additional $5 billion in EBITDA.

How Did the Stock React?

BHP shares traded up 0.85% to $73.38 on the day of the earnings release, adding to the strong performance since the prior half. The stock is trading near its 52-week high of $75.14, reflecting investor confidence in the copper-centric growth strategy.

The muted immediate reaction suggests much of the operational strength was anticipated, though the $10 billion capital unlocking announcement adds a new catalyst.

What Did Management Guide?

Near-Term Outlook

Management expressed confidence in meeting full-year guidance across the business:

- Iron Ore: On track to reach 305 million tons per year by end of FY28, with path to 330 million tons if market conditions warrant

- Copper: Targeting 2.5 million tons copper equivalent per year by mid-2030s

- Cost Leadership: Iron ore costs targeted below $17.50/ton in medium term (10% reduction)

Cash Flow Guidance

At spot commodity prices, BHP expects to generate approximately $60 billion in attributable free cash flow over the next five years—after funding all growth investments.

Even in an "extreme and prolonged low-price environment" (prices 20-40% below current levels for five years), the company would still generate around $10 billion in attributable free cash flow.

Key Management Quotes

Mike Henry, CEO, on copper's strategic importance:

"Just over half of our earnings for the period came from our copper business. That's up 30 percentage points over the past three years, and this is the result of our deliberate actions to grow our copper business."

Vandita Pant, CFO, on the capital unlocking strategy:

"These agreements are examples of BHP's razor-sharp approach to capital portfolio and asset management. They improve our financial flexibility, unlock value, and benefit BHP's shareholders."

Mike Henry on the growth opportunity:

"Global demand for copper is projected to grow by around 70% between 2021 and 2050. That demand is durable and multifaceted—traditional economic growth, the energy transition, and the need for data centers to support increasing use of artificial intelligence."

Growth Pipeline: From Stability to Acceleration

BHP outlined a clear production growth trajectory: ~3% per year through 2030, accelerating beyond. The copper business alone is expected to grow ~5% per year on average.

Key Growth Projects

Jansen Update

Management acknowledged updated cost estimates for Jansen Stage 1 to $8.4 billion, maintaining the mid-2027 first production timeline. Once ramped up, Jansen is expected to deliver margins above 60% and provide portfolio diversification from different demand drivers and customer markets.

Commodity Market Outlook

Management's view on near-term demand:

- Global GDP: Expected broadly in line with 2025, supported by policy responses

- China: 15th Five-Year Plan expected to lift domestic household demand and prioritize technological development

- India: Positive momentum continuing with infrastructure investment and manufacturing expansion

- Supply: Combined with tight supply, fundamentals for BHP's commodities remain supportive

Risks and Concerns Flagged

While the results were strong, several risks were noted:

- Policy Uncertainty: Continued policy and geopolitical uncertainty could influence investment and trade flows

- Iron Ore Competition: Management acknowledged "fiercer competition" in iron ore markets as the steel industry evolves

- Project Execution: The Jansen cost overrun highlights execution risk on major projects

- Commodity Price Volatility: Results heavily influenced by commodity price environment

The Bottom Line

BHP delivered a strong first half that validates its multi-year strategy to pivot toward copper while maintaining cost leadership in iron ore. The record copper performance—now generating majority earnings—positions the company for secular growth in electrification and AI infrastructure.

The $10 billion capital unlocking initiative provides ammunition for either accelerated growth or enhanced shareholder returns, demonstrating management's focus on capital productivity. With $60 billion in projected free cash flow over five years at spot prices, BHP offers investors both defensiveness and growth exposure.

The 46% dividend increase signals confidence, though the updated Jansen cost estimate reminds investors that major project execution remains a monitoring point.